Tax Audit Applicability under Section 44AB – Understanding the Threshold Limits for FY 2025-26 (AY 2026-27)

Jun 25, 2026

Tax Audit is one of the most significant compliance requirements under the Income-tax Act, 1961. However, a common misconception among taxpayers is that every business or professional exceeding a certain turnover must undergo a tax audit. Over the years, the Government has introduced higher threshold limits and presumptive taxation schemes to reduce the compliance burden, particularly for small businesses and professionals.

Understanding the applicability of tax audit is essential to ensure timely compliance while avoiding unnecessary audits and penalties.

What is a Tax Audit?

A Tax Audit under Section 44AB is an examination of a taxpayer's books of accounts by a Chartered Accountant to ensure that the accounts are properly maintained and comply with the provisions of the Income-tax Act.

The objective is to:

- Ensure accuracy of financial records

- Verify compliance with tax laws

- Detect reporting inconsistencies

- Facilitate correct computation of taxable income

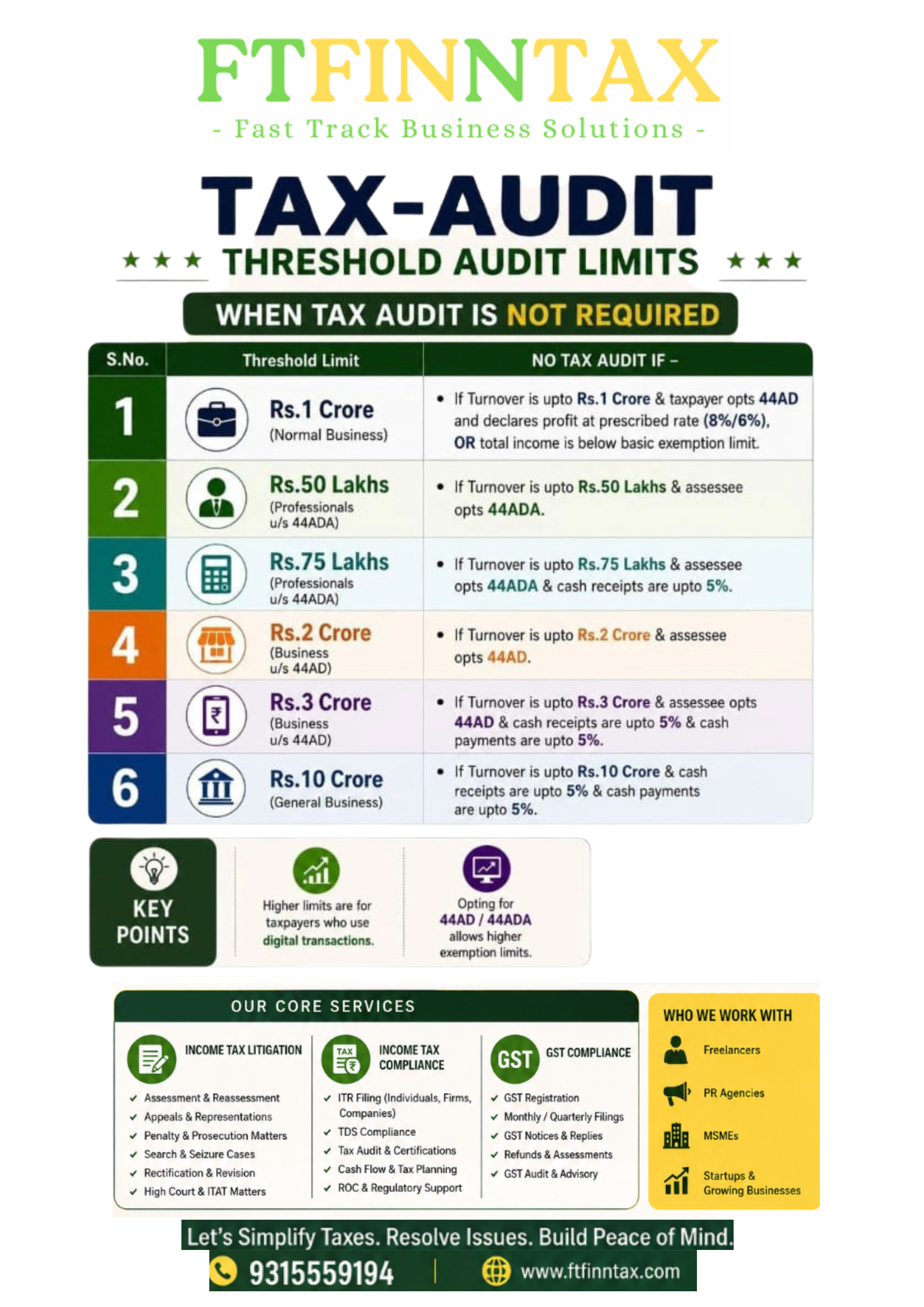

Tax Audit Threshold Limits for FY 2025-26 (AY 2026-27)

1. Normal Business – Turnover up to ₹1 Crore

A person carrying on business is generally required to get accounts audited if turnover exceeds ₹1 Crore.

However, no tax audit is required if:

- Turnover is up to ₹1 Crore; or

- The taxpayer opts for Section 44AD and declares profit at the prescribed rate (8%/6%); or

- Total income does not exceed the basic exemption limit (subject to provisions of Section 44AD).

2. Professionals opting for Section 44ADA – Gross Receipts up to ₹50 Lakhs

Specified professionals such as:

- Chartered Accountants

- Doctors

- Lawyers

- Architects

- Engineers

- Interior Decorators

- Technical Consultants

can opt for the presumptive taxation scheme under Section 44ADA if gross receipts do not exceed ₹50 Lakhs.

By declaring at least 50% of gross receipts as income, they are not required to maintain detailed books or undergo tax audit.

3. Professionals with Gross Receipts up to ₹75 Lakhs

The Finance Act has increased the limit to ₹75 Lakhs, provided:

- Cash receipts do not exceed 5% of total receipts.

This encourages digital transactions while reducing compliance costs for professionals.

4. Businesses opting for Section 44AD – Turnover up to ₹2 Crores

Eligible businesses can opt for Section 44AD if turnover does not exceed ₹2 Crores.

Income is presumed at:

- 8% of turnover (cash receipts)

- 6% of digital receipts

No tax audit is required if the taxpayer complies with the provisions of Section 44AD.

5. Businesses with Turnover up to ₹3 Crores

The turnover limit under Section 44AD has been enhanced to ₹3 Crores, provided:

- Cash receipts do not exceed 5%

- Cash payments do not exceed 5%

This benefit is available only to businesses adopting digital transactions.

6. General Business – Turnover up to ₹10 Crores

Even if a taxpayer is not opting for presumptive taxation, tax audit under Section 44AB is not required up to ₹10 Crores where:

- Cash receipts do not exceed 5% of total receipts; and

- Cash payments do not exceed 5% of total payments.

This relaxation was introduced to promote a digital economy and reduce compliance costs.

Summary of Tax Audit Limits

|

Category |

Threshold |

Tax Audit Not Required When |

|

Normal Business |

₹1 Crore |

Turnover within limit or eligible under Section 44AD |

|

Professionals (44ADA) |

₹50 Lakhs |

Opting for Section 44ADA |

|

Professionals (Digital) |

₹75 Lakhs |

Cash receipts ≤ 5% |

|

Business (44AD) |

₹2 Crores |

Opting for Section 44AD |

|

Business (Digital 44AD) |

₹3 Crores |

Cash receipts & payments ≤ 5% |

|

General Business |

₹10 Crores |

Cash receipts & payments ≤ 5% |

Benefits of Higher Tax Audit Limits

The enhanced thresholds provide several advantages:

- Reduced compliance burden

- Lower audit and professional costs

- Simplified tax filing

- Encouragement for digital transactions

- Improved ease of doing business

- Better focus on business growth rather than regulatory compliance

Important Points Taxpayers Should Remember

- Tax audit applicability depends not only on turnover but also on the nature of business, presumptive taxation provisions, and the percentage of cash transactions.

- Businesses opting out of presumptive taxation after previously opting for it may still become liable for tax audit under specific circumstances.

- Certain taxpayers may require tax audit due to other provisions of the Income-tax Act even if turnover is below these limits.

- Proper maintenance of books and documentation remains essential, irrespective of whether tax audit is applicable.

Conclusion

The Government has significantly liberalised the tax audit provisions by introducing higher threshold limits for businesses and professionals, particularly those embracing digital transactions. These amendments aim to simplify tax compliance, reduce the cost of doing business, and promote a cashless economy.

However, determining tax audit applicability is not merely a matter of checking turnover. Taxpayers must carefully evaluate the relevant provisions of Sections 44AB, 44AD, and 44ADA, along with the conditions relating to cash receipts and cash payments.

Before concluding that a tax audit is not required, it is advisable to seek professional guidance to ensure complete compliance with the Income-tax Act and avoid future litigation.

Need help determining whether

your business requires a Tax Audit?

📞 93155 59194

📧 ftfinntaxconsultants@gmail.com

🌐 www.ftfinntax.com