Surge in Income Tax Scrutiny Notices Under Section 143(2): What Taxpayers Need to Know

Jun 25, 2026

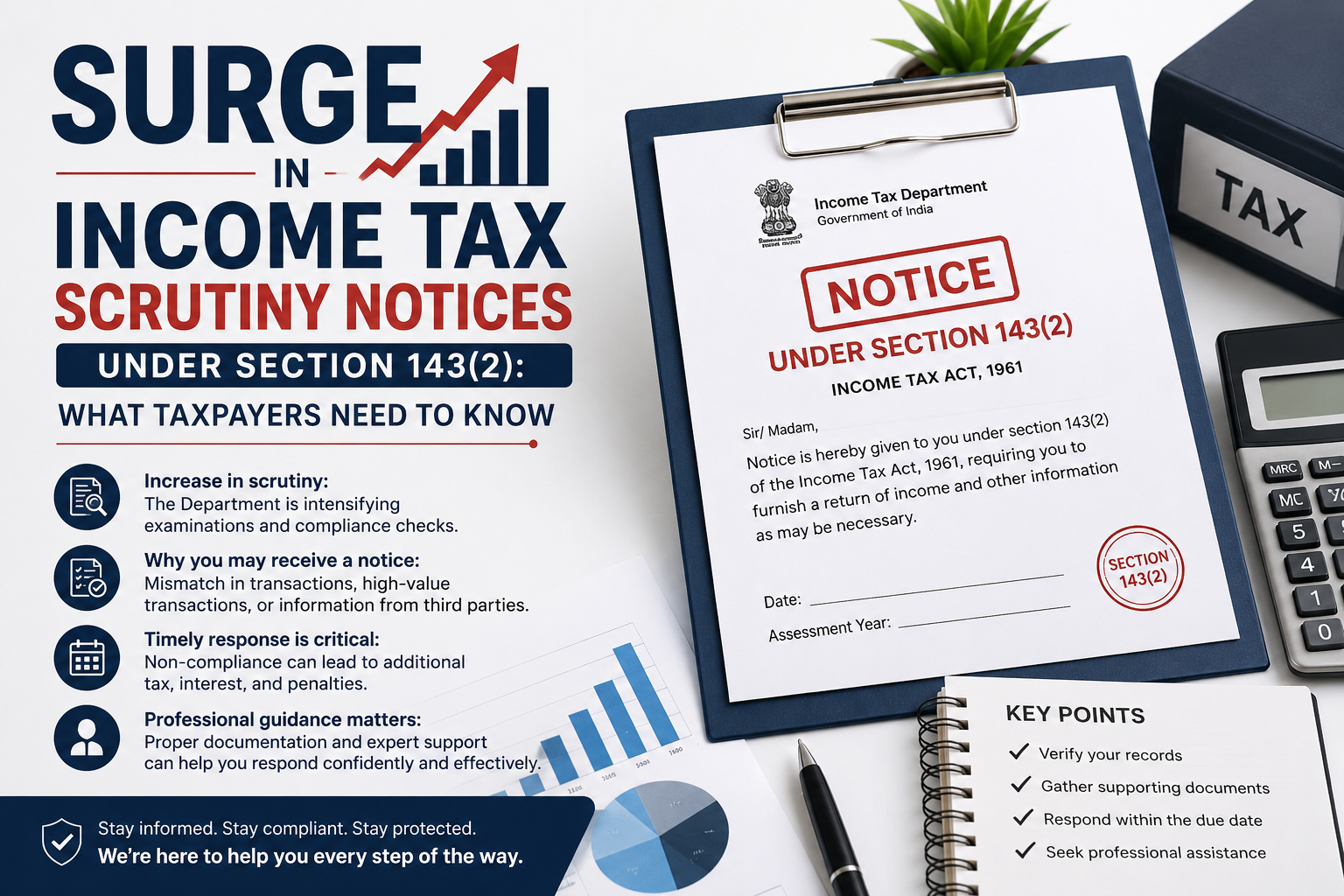

Over the last few days, it appears that the Income Tax Department has issued a significant number of scrutiny notices under Section 143(2) of the Income-tax Act. Many taxpayers and professionals have reported receiving such notices, leading to understandable concern and confusion.

If you have received a notice under Section 143(2), the first and most important thing to remember is:

- Receiving a scrutiny notice does not automatically mean that there is any tax evasion, concealment, or wrongdoing.

The notice simply indicates that the Income Tax Department has selected your return for detailed examination and verification.

What is a Notice Under Section 143(2)?

A notice under Section 143(2) is issued when the Income Tax Department wishes to scrutinize a return filed by a taxpayer. The objective is to verify the correctness of:

- Income declared in the return

- Deductions and exemptions claimed

- Tax credits and TDS reported

- Capital gains disclosures

- Business and professional income

- High-value financial transactions

- Other information available with the department

The scrutiny process is now largely conducted through the Faceless Assessment Scheme, ensuring greater transparency and minimizing direct interaction with tax authorities.

Why Might a Return Be Selected for Scrutiny?

While the exact selection criteria are not publicly disclosed, returns may be picked for scrutiny due to:

1. High-Value Transactions

Transactions such as:

- Large cash deposits

- Significant property purchases or sales

- High-value investments

- Foreign remittances

may trigger verification.

2. Mismatch in Information

Differences between:

- ITR and Form 26AS

- ITR and AIS/TIS

- Books of accounts and tax filings

can attract scrutiny.

3. Unusual Claims

Large deductions, exemptions, losses, or refunds compared to past years may require additional verification.

4. Risk-Based Selection

The department uses data analytics and AI-based risk parameters to identify cases requiring examination.

What Should You Do If You Receive Such a Notice?

Do Not Panic

Many taxpayers become anxious immediately after receiving a notice. However, a scrutiny notice is a procedural step and should be handled professionally.

Review the Notice Carefully

Understand:

- Assessment Year involved

- Response deadlines

- Specific issues raised by the department

- Documents required

Gather Supporting Documents

Maintain proper documentation such as:

- Bank statements

- Books of accounts

- Purchase and sale deeds

- Investment proofs

- Tax deduction certificates

- Agreements and supporting evidence

Respond Within Time

Ignoring a notice can lead to adverse consequences. Timely and accurate compliance is essential.

Seek Professional Guidance

A well-drafted and fact-based response can significantly improve the outcome of scrutiny proceedings.

Common Mistakes Taxpayers Should Avoid

❌ Ignoring the notice

❌ Submitting incomplete information

❌ Providing inconsistent explanations

❌ Responding without understanding the issue raised

❌ Missing statutory deadlines

The Right Approach

A scrutiny assessment should be viewed as an opportunity to explain and substantiate the information already disclosed in the return. With proper documentation, professional representation, and timely compliance, most scrutiny proceedings can be handled effectively.

If you have recently received a notice under Section 143(2) and would like guidance regarding:

- Understanding the notice

- Preparing a response

- Documentation requirements

- Faceless assessment proceedings

- Assessment strategy and representation

feel free to connect or send me a message.

Remember:

A notice is not a problem. An unaddressed notice can become one.